Wash Sales with Multiple SMA Managers

We’re coming off of one of the sharpest equity market rallies in recent memory. Since the April 7 inter-day low, the S&P 500 has climbed over 16% — that’s a powerful recovery that’s called into question the forward direction of the economy.

So what’s behind this move? In part, it is a function of adjusting expectations. Markets had priced in a worst-case scenario on trade policy, growth and earnings. And while those risks haven’t disappeared, the incoming data has been more balanced than feared.

At the same time, we’re seeing a market that’s reacting more to good news and discounting bad news, at least for now. And that dynamic creates a different kind of risk, one of overshooting on relief. And it’s a reminder that staying grounded in long-term fundamentals matters more than ever.

So let’s start with where we are in the economy.

■ Previous Month ■ Current Month

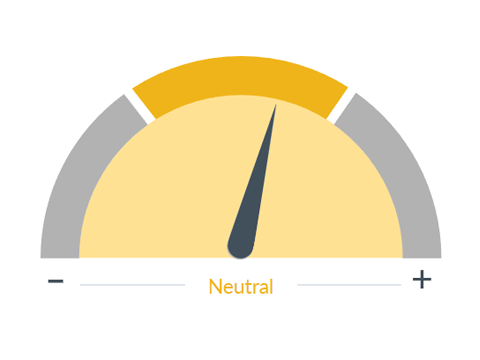

US Economic Outlook

What we see

City National Rochdale utilizes a comprehensive internal research effort that is complemented by an extensive set of external research from some of Wall Street's leading strategists. This approach allows us to develop a complete and dependable forecast of economic conditions. Our economic outlook indicator provides our forecasted expectation for how well the U.S. economy will perform over the next 3-6 months.

Dial 1: U.S. Economic Outlook, 0:57— The initial Q1 GDP report showed a mild contraction of -0.3%. That’s the first negative print since early 2022. That headline number did raise some eyebrows, but when we look under the hood, the story is more nuanced and, in our view, more constructive.

The decline was primarily driven by a historic surge in imports as businesses scrambled to front-run new tariffs. That drag from net exports covered up what was otherwise a pretty good report. In fact, real final sales to private domestic purchasers — now that’s just a fancy term for a core measure of underlying demand — rose about 3% in Q1. That tells us that consumers and businesses are still spending and investing. While growth is clearly slowing, the foundation remains intact. It’s a mixed message, yes, but not a recessionary one.

On the labor front, April’s nonfarm payroll report confirmed that the job market is not yet under pressure.

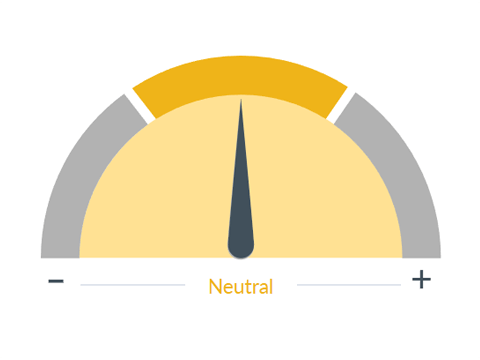

■ Previous Month ■ Current Month

Labor Market

What we see

Research has shown that employment and income expectations, along with credit availability, are the most important determinants of consumer spending. Personal consumption amounts to roughly 70% of GDP, making a strong labor market essential to a healthy economy.

Dial 2: Labor Market, 1:49— The economy added about 252,000 jobs, surpassing expectations and marking another month of steady hiring. The unemployment rate held steady, and participation continued to trend up, both encouraging signs. But it also complicates the Fed’s job, as they attempt to limit the inflationary impact of tariffs while simultaneously watching out for any negative impacts to the job market. So for now, we believe they will not adjust policy until they have more clarity on one or both of these mandates.

That said, we are beginning to see early impacts from the Department of Government Efficiency’s workforce reductions. It’s estimated that over 200,000 federal positions have been cut in recent months. And while that’s a small piece of the overall labor picture, it’s something that we’re monitoring closely, particularly for second-order effects on regional economies and contract workers.

Now shifting the focus back to the markets, earning season for the S&P 500 has been notably strong, with earnings growing by about 12.8% year over year. That marks the second consecutive quarter of double-digit earnings growth and the seventh straight quarter of overall gains. Approximately 76% of reporting companies have exceeded earnings estimates, and revenue growth now stands at about 4.8%, with 62% of companies surpassing sales expectations.

Sectors such as health care, communication services and information technology have led the earnings growth, while the energy sector has struggled with lower crude oil prices. And overall, despite these positive results, many companies are issuing cautious guidance or withdrawing it altogether due to uncertainties surrounding tariffs and policy changes. Now that indicates a prudent approach to future projections, but it also underscores the importance of tariff resolution.

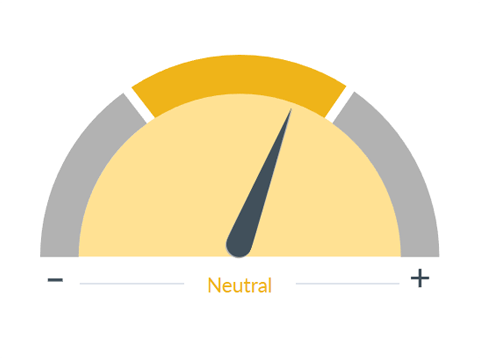

■ Previous Month ■ Current Month

Monetary Policy

What we see

Monetary policy is one of two ways the government can influence the economy and financial markets. By manipulating interest rates, the Federal Reserve can raise or lower the cost of money to stabilize or stimulate the economy.

Dial 3: Monetary Policy, 3:28— So turning to policy, the tariffs announced earlier this year were a shock to the system, and we’re now starting to see some of the early downstream effects. But importantly, this is not a financial crisis. We don’t see a systemic breakdown, there’s no excess leverage, and there’s no structural imbalance. Instead, we’re seeing how firms and consumers adapt to a new set of rules. Administration officials, including Scott Bessent, the Treasury secretary, have laid out an economic vision that centers on tariffs, tax incentives and deregulation as tools to reshape supply chains and restore domestic investment.

So whether one agrees with the strategy or not, the intent overall might not be wrong, and that’s to create a more self-reliant and resilient economic base in the U.S., and encouragingly, there are some signs of potential easing on the trade front. While rhetoric remains firm, reports suggest that back-channel discussions are underway with key trading partners, and the possibility of targeted exemptions or bilateral agreements in certain sectors are definitely live. China has floated the idea of resuming formal negotiations, and exemptions for some U.S. goods have been quietly reinstated.

It’s too early to count on a broad de-escalation, but the door is certainly not closed to one. And as for our Speedometers®, there were no changes this month. While the underlying environment remains uncertain, the data does not yet warrant additional shifts in positioning.

Broadly speaking, the Speedometer® changes we made last month point to a macro picture that remains mixed but stable. Economic growth is slowing but not stalling. The labor market is holding up as we discussed. Inflation pressures are elevated, but they’re largely explainable through policy pass-through. And while two committee members expressed a slightly more cautious view on the housing market, there was not a consensus for a formal downgrade. So we believe it’s appropriate to maintain a steady stance while closely monitoring how policy and fundamentals evolve.

So what’s the key takeaway this month for investors?

This is a time to remain focused and thoughtful. The recent rally has created breathing room and an opportunity to reassess exposures, potentially rebalance portfolios and position for a range of outcomes. It’s not a time to chase momentum or overreact to short-term headwinds. Just as the market overshot to the downside earlier this year, it may now be leaning too far in the other direction.

So we believe that staying grounded in long-term fundamentals and being deliberate in how portfolios evolve is the best path forward. Our role is to help you navigate these uncertain periods with clarity and composure. That means being proactive, not reactive, and making sure that every portfolio decision is tied to the right time horizon and risk tolerance.

So we’ll continue to watch the data closely.

When the environment truly shifts, whether that’s a resolution on tariffs, a new tone from the Fed or a change in corporate earning strengths, we’ll be ready to adjust accordingly. In the meantime, we remain focused on stability and long-term growth and helping you reach your investment goals with confidence.

The information presented does not involve the rendering of personalized investment, financial, legal or tax advice. This presentation is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein.

Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results and are based primarily upon a hypothetical set of assumptions applied to certain historical financial information. Certain information has been provided by third-party sources and, although believed to be reliable, it has not been independently verified and its accuracy or completeness cannot be guaranteed.

Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change.

CNR Speedometers® are indicators that reflect forecasts of a 6-to-9-month time horizon. The colors of each indicator, as well as the direction of the arrows represent our positive/negative/neutral view for each indicator. Thus, arrows directed towards the (+) sign represents a positive view which in turn makes it green. Arrows directed towards the (-) sign represents a negative view which in turn makes it red. Arrows that land in the middle of the indicator, in line with the (0), represents a neutral view which in turn makes it yellow. All of these indicators combined affect City National Rochdale’s overall outlook of the economy.

City National, its managed affiliates and subsidiaries, as a matter of policy, do not give tax, accounting, regulatory, or legal advice, and any information provided should not be construed as such.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

City National Rochdale, LLC, is a SEC registered investment adviser and wholly owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank and City National Rochdale are subsidiaries of Royal Bank of Canada.

©2025 City National Rochdale, LLC. All rights reserved.

NON-DEPOSIT INVESTMENT PRODUCTS ARE: • NOT FDIC INSURED •NOT BANK GUARANTEED •MAY LOSE VALUE