Videos › Fixed Income Perspectives › February 2026

-

Fixed Income Perspectives

Bonds “Carry” Investors Through Volatility

February 2026

- Filename

- Fixed Income Perspectives February 2026.pptx

- Format

- application/vnd.openxmlformats-officedocument.presentationml.presentation

TRANSCRIPT

Fixed income markets confronted a mix of geopolitical tensions and policy uncertainty to start the year. Volatility re-emerged as investors digested concerns over Venezuela and Greenland as well as renewed threats over Fed independence just to name a few. As expected, the FOMC kept the overnight lending rate unchanged at their January meeting and signaled no hurry for further easing in the near term. The market will be more preoccupied with the nomination of Kevin Warsh to lead the Fed than it will be with actual policy implementation for the next few months. From a fundamental perspective, data has shown the economy is on firmer footing than expected, but lingering worries about the labor market remain.

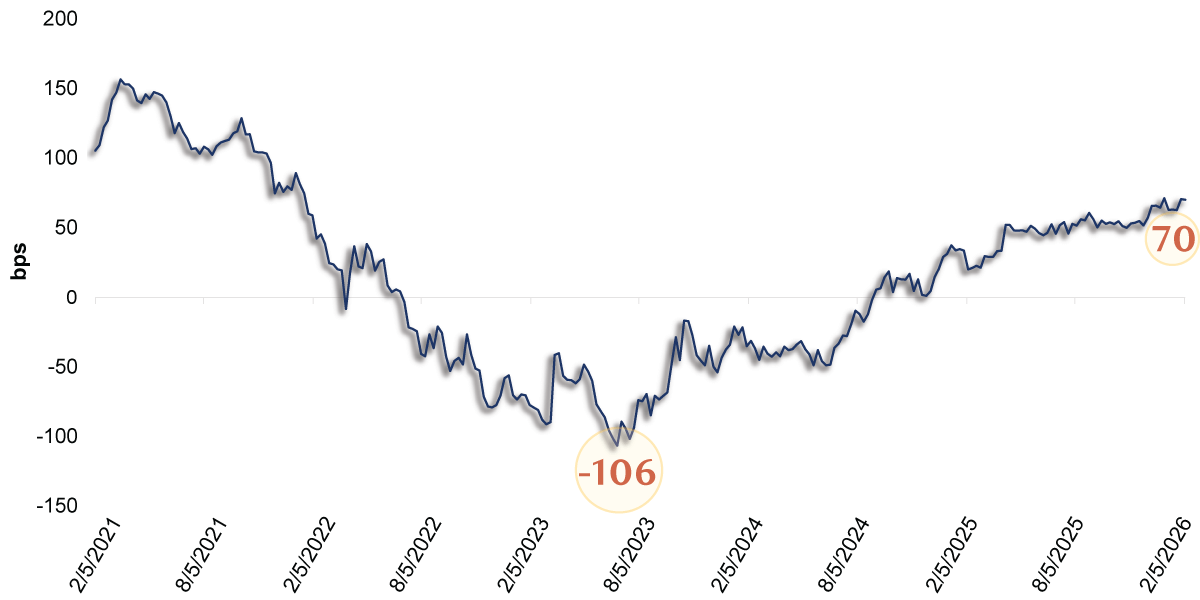

Treasury 2/10 Spread

Source: Bloomberg US Treasury 2-10 Spread Index as of 2/9/2026.

Information is subject to change and is not a guarantee of future results.

Chart 1, 0:58– Despite this volatility, the bond market continues to remain stable. After a push higher in yields that saw the 10-year Treasury reach a five-month high of 4.29%, volatility has given way to a market that has refocused on fundamentals. Rates have once again retreated from recent highs, and the yield curve has steepened. The yield differential between 2-year and 10-year treasuries is now just over 70 bps - the steepest in over four years suggesting growing confidence the Fed will resume rate cuts while longer maturities will stay elevated.

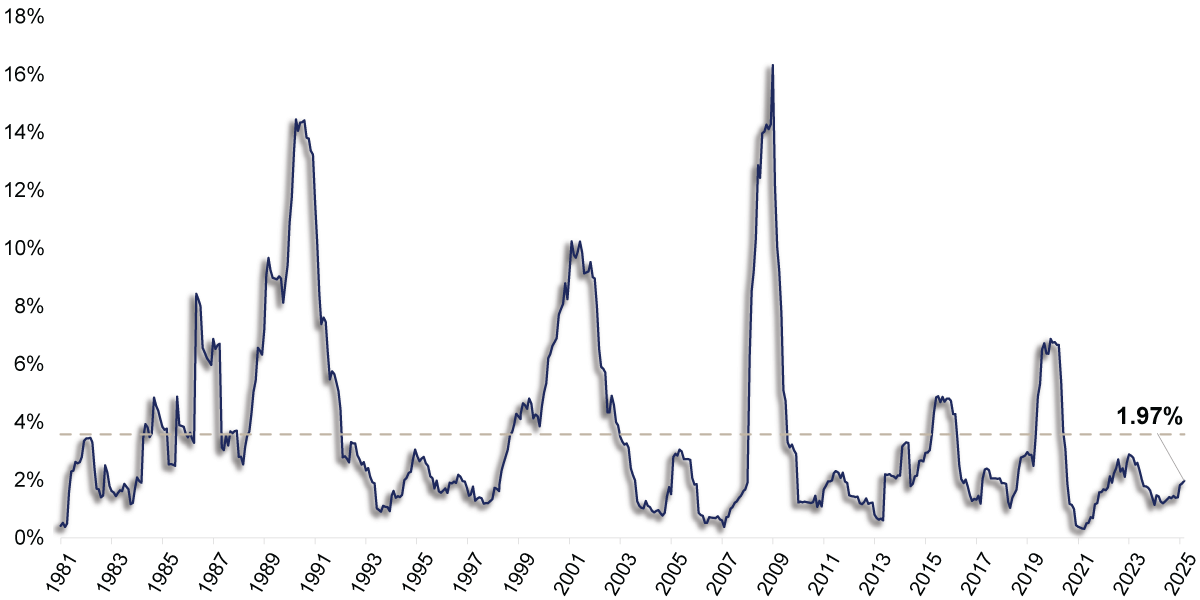

Long-Term Corporate Default Rates

Source: RBC Rochdale Research as of 1/31/2026.

Past performance is not a guarantee of future results.

Chart 2, 1:35– Policy- and geopolitical-driven volatility in the U.S. Treasury market has been met with a divergent response in corporate credit markets. Despite elevated uncertainty, the compensation investors require for assuming credit risk—measured by credit spreads— has compressed to cyclical lows within the investment-grade sector and remains historically low in high yield. Although yields are below levels observed a year ago, they remain attractive in absolute terms. Credit fundamentals are stable, supported by moderate leverage, strong interest-coverage ratios, and default rates that continue to run below long-term averages. While valuations appear full and security selection is increasingly important, the prospect of near-term fiscal stimulus from tax policy changes is a supportive factor for corporate credit markets in the near-term. Municipal bonds have also started the year largely unaffected by geopolitical volatility, carrying forward momentum that developed in the second half of last year. Technicals have been a primary driver with heavy and persistent investor demand from principal redemptions, coupon payments and new money.

Technicals Drive Strong Municipal Performance

Source: Bloomberg Muni and Treasury Yield Curves, Bloomberg US Treasury Index, Bloomberg Municipal Bond Index, Bloomberg Intermediate US Treasury Index, Bloomberg Short Intermediate Municipal Bond Index, Bloomberg Short US Treasury Index, Bloomberg Short Municipal Bond Index as of 2/9/2026.

Past performance is not a guarantee of future results.

Chart 3, 2:47– This has primarily concentrated interest in short and intermediate maturities. As a result, municipal yields moved sharply lower to start the year, and while only a month into the year, municipals have emerged as one of the best-performing markets within fixed income. Here again, valuations are tight but supported by strong credit fundamentals. Although yields remain historically attractive, we remain cautious, as expectations for heavier supply later in the quarter could begin to weigh on market performance. Despite a volatile start to the year, bond markets continue to show resilience. Our baseline case is that firming growth and easing inflation will continue to support stable credit conditions and point to a steeper yield curve. Our outlook is for the Fed to resume rate cuts later this year and for longer-term treasuries to remain rangebound with 10-year yields centered around 3.75-4.25. Though lower than the start of 2025, yields remain attractive on a historical basis, and we believe coupon income will drive returns for much of the year.

Important Information

The views expressed represent the opinions of RBC Rochdale, LLC which are subject to change and are not intended as a forecast or guarantee of future results. Stated information is provided for informational purposes only, and should not be perceived as personalized investment, financial, legal or tax advice or a recommendation for any security. It is derived from proprietary and non-proprietary sources which have not been independently verified for accuracy or completeness. While RBC Rochdale believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Actual results, performance or events may differ materially from those expressed or implied in such statements.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met, and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

RBC Rochdale, LLC is an SEC-registered investment adviser and wholly-owned subsidiary of City National Bank. Registration as an investment adviser does not imply any level of skill or expertise. City National Bank is a subsidiary of the Royal Bank of Canada.

Fixed Income investing strategies & products. There are inherent risks with fixed income investing. These risks include, but are not limited to, interest rate, call, credit, market, inflation, government policy, liquidity or junk bond risks. When interest rates rise, bond prices fall. This risk is heightened with investments in longer-duration fixed income securities and during periods when prevailing interest rates are low or negative.

High yield securities. Investments in below-investment-grade debt securities, which are usually called “high yield” or “junk bonds,” are typically in weaker financial health. Such securities can be harder to value and sell, and their prices can be more volatile than more highly rated securities. While these securities generally have higher rates of interest, they also involve greater risk of default than do securities of a higher-quality rating.

© 2026 RBC Rochdale, LLC. All rights reserved.

Index Definitions:

Bloomberg Muni and Treasury Yield Curves are graphical representations showing the relationship between interest rates (yields) and time to maturity for tax-exempt municipal bonds and taxable U.S. Treasury securities, respectively.

Bloomberg US Treasury Index measures the performance of U.S. dollar-denominated, fixed-rate, nominal debt issued by the U.S. Treasury, excluding Treasury bills, inflation-linked bonds, and STRIPS. It includes public obligations with at least one year remaining to maturity and is a key component of the broader Bloomberg Aggregate Index.

Bloomberg Municipal Bond Index is a rules-based, market-value-weighted index that measures the performance of the USD-denominated, investment-grade, long-term tax-exempt bond market.

Bloomberg Intermediate US Treasury Index measures the performance of U.S. dollar-denominated, fixed-rate, nominal debt issued by the U.S. Treasury with a remaining maturity of 1 to 10 years.

Bloomberg Short US Treasury Index measures the performance of U.S. dollar-denominated, fixed-rate, nominal debt issued by the U.S. Treasury with a remaining maturity of less than one year (specifically 1 month up to 1 year).

Bloomberg Short Municipal Bond Index is a market value-weighted index tracking investment-grade, tax-exempt U.S. municipal bonds with short-term maturities, typically ranging from one to five years.

Stay Informed.

Get our Insights delivered straight to your inbox.

Put our insights to work for you.

If you have a client with more than $1 million in investable assets and want to find out about the benefits of our intelligently personalized portfolio management, speak with an investment consultant near you today.

If you’re a high-net-worth client who's interested in adding an experienced investment manager to your financial team, learn more about working with us here.